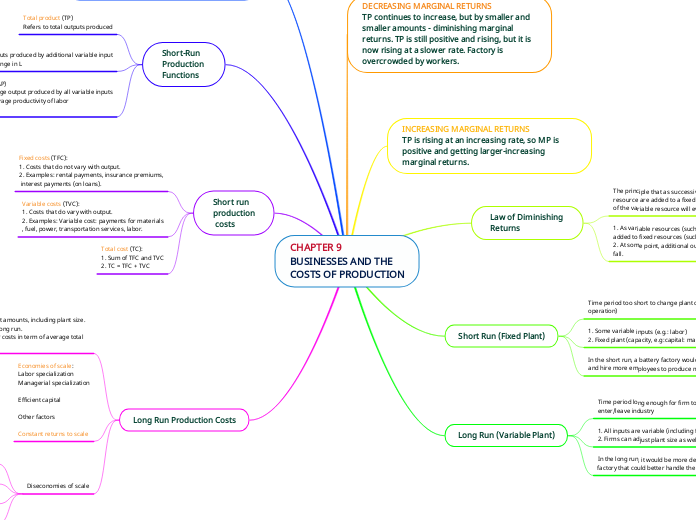

CHAPTER 9

BUSINESSES AND THE

COSTS OF PRODUCTION

DECREASING MARGINAL RETURNS

TP continues to increase, but by smaller and smaller amounts - diminishing marginal returns. TP is still positive and rising, but it is now rising at a slower rate. Factory is overcrowded by workers.

INCREASING MARGINAL RETURNS

TP is rising at an increasing rate, so MP is positive and getting larger-increasing marginal returns.

Law of Diminishing

Returns

The principle that as successive increments of a variable resource are added to a fixed resource, the marginal product of the variable resource will eventually decrease.

1. As variable resources (such as labor) are continuously added to fixed resources (such as machines),

2. At some point, additional output (marginal product, MP) will fall.

Short Run (Fixed Plant)

Time period too short to change plant capacity (size of operation)

1. Some variable inputs (e.g.: labor)

2. Fixed plant (capacity, e.g:capital: machines, factory size)

In the short run, a battery factory would purchase more inputs and hire more employees to produce more batteries.

Long Run (Variable Plant)

Time period long enough for firm to adjust plant capacity and enter/leave industry

1. All inputs are variable (including factory size)

2. Firms can adjust plant size as well as enter and exit industry.

In the long run, it would be more desirable to build a new factory that could better handle the increased production.

NEGATIVE MARGINAL RETURNS

TP falls and MP becomes negative. Additional worker reduces total outputs. Too many workers are hired.

Short-Run

Production

Functions

Total product (TP)

Refers to total outputs produced

Marginal product (MP)

Refers to additional outputs produced by additional variable input

MP = Change in TP / Change in L

Average product (AP)

Refers to the average output produced by all variable inputs

Also called the average productivity of labor

AP = TP / L

Short run

production

costs

Fixed costs (TFC):

1. Costs that do not vary with output.

2. Examples: rental payments, insurance premiums,

interest payments (on loans).

Variable costs (TVC):

1. Costs that do vary with output.

2. Examples: Variable cost: payments for materials

, fuel, power, transportation services, labor.

Total cost (TC):

1. Sum of TFC and TVC

2. TC = TFC + TVC

Long Run Production Costs

1. The firm can change all input amounts, including plant size.

2. All costs are variable in the long run.

3. Long run ATC: Now consider costs in term of average total costs.

Economies of scale:

Labor specialization

Managerial specialization

Efficient capital

Other factors

Constant returns to scale

Diseconomies of scale

control and coordination problems

Communication problems

Worker alienaton

Shirking