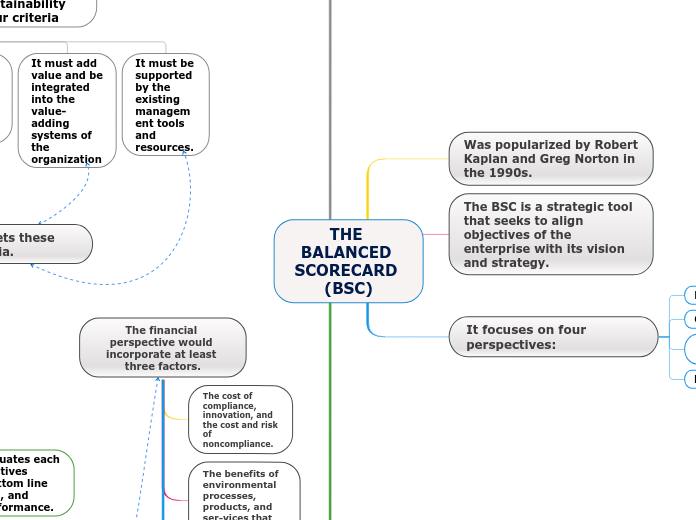

THE BALANCED SCORECARD (BSC)

INCORPORATING SUSTAINABILITY INTO THE BSC

Any attempt to measure success in sustainability must meet four criteria

It must address the triple bottom line of sustainability: economic, social, and environmental performance

It must have performance measures that can be clearly understood and communicated

It must add value and be integrated into the value-adding systems of the organization

It must be supported by the existing management tools and resources.

HOW TO INCORPORATE SUSTAINABILITY INTO THE BSC.

Three approaches have been utilized

The first approach integrates environmental and social aspects into the existing perspectives

This approach does not appear to have gained much use in practice

The second approach adds an additional perspective to the existing four in order to incorporate environmental and social aspects

Referred to as the “nonmarket perspective,” this approach is seen as necessary because environmental and social issues are not fully integrated into the market exchange process.

The third approach develops a separate scorecard, which is referred to as the sustain-ability balanced scorecard (SBSC).

This approach evaluates each of the four perspectives along the triple bottom line of economic, social, and environmental performance.

Was popularized by Robert Kaplan and Greg Norton in the 1990s.

The BSC is a strategic tool that seeks to align objectives of the enterprise with its vision and strategy.

It focuses on four perspectives:

FINANCIAL

CUSTOMER

INTERNAL BUSINESS PROCESSES

LEARNING AND GROWTH