Accounting -The keeping and processing of financial information in order to make decisions based on it.

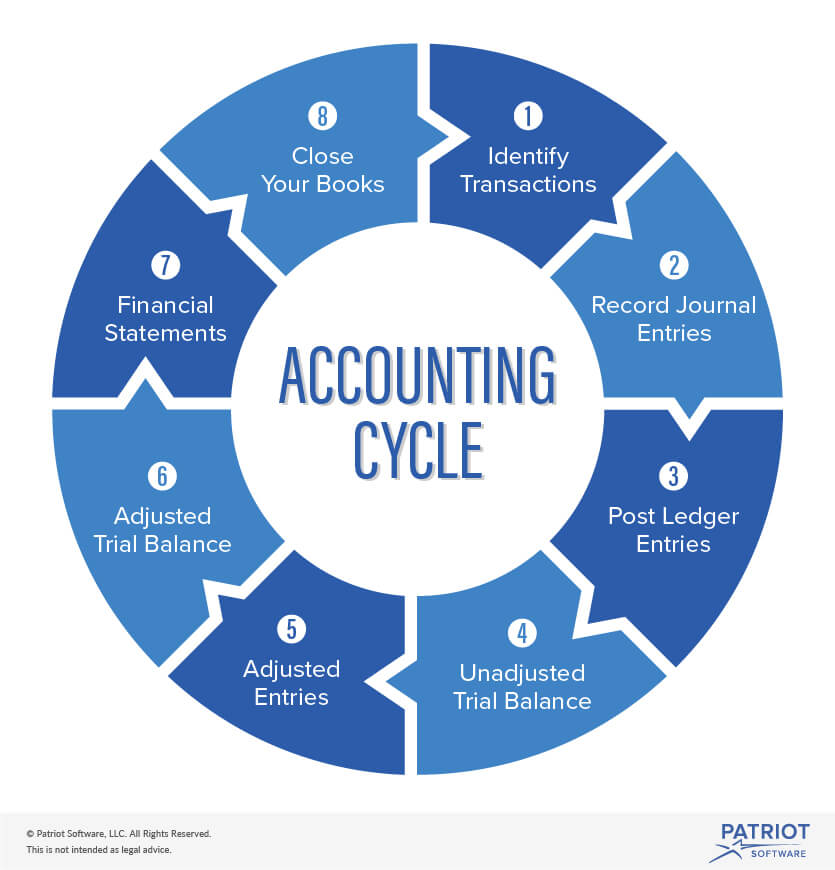

Accounting Cycle -The process of identifying, analyzing and recording transactions and financial data of a company. There are 8 steps. 1.Originating Transaction Data-Identifying transactions that took place 2.Journalizing-Recording the transactions as journal entries 3.Posting-The transactions are posted in the general ledger 4.Trial Balance-A Trial balance is made to make sure the credits and debits are equal 5.Worksheet-A worksheet is made to check that the debits and credits are equal. If they are not equal then adjustments need to be made to make them equal 6.Financial Statements-A modified trial balance and financial statements 7.Closing Entries-The accounts are finalized and the net income is turned into earnings for the end of the period 8.Post-closing Trial Balance-A trial balance is made to make sure the debits and credits are equal and then the cycle begins again

GAAP (Generally Accepted Accounting Principles) -Rules, practices and procedures that all accounts need to follow. Principle of regularity-Accountants must follow the rules and regulations Principle of consistency-The financial reporting process has consistent standards throughout Principle of sincerity-Accounts must be honest and impartial Principle of performance of methods-When preparing financial reports consistent procedures are used Principle of non-compensation-Every aspect of a company's performance is reported with no prospect of debt compensation Principle of prudence-Financial reporting is not influenced by speculation Principle of continuity-It is assumed the business will keep going Principle of periodicity-The reporting of revenue is made at consistent intervals of time Principle of materiality-Financial reports fully disclose the financial situation of the company Principle of utmost good faith-It is assumed all parties are honest

Financial statements -Written reports that convey a company's transactions and performance. They are used to make decisions or in case the company is audited.

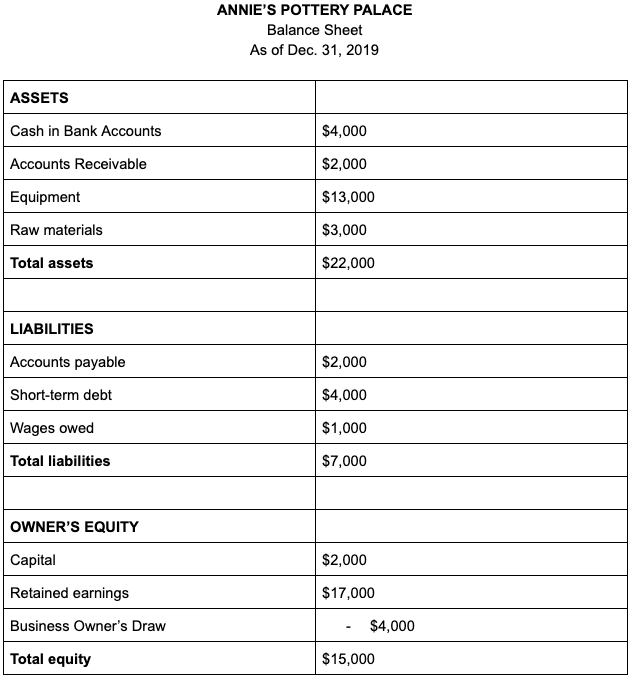

Balance Sheet -A sheet that shows a company's or person's assets, liabilities and owner's equity.

Financial Position -The balances of a company's or individual's assets, liabilities and equity.

Assets -Resources of a company or person that have monetary value.

Liabilities -Debts and obligations a company or person has to pay back.

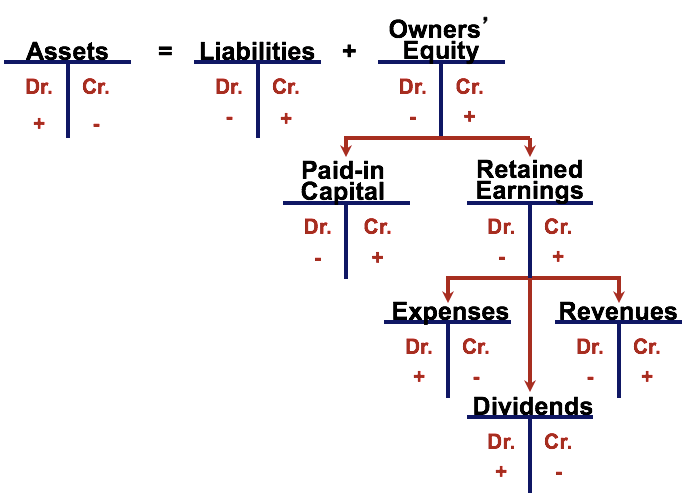

Owner's Equity -The owner's claim on the total assets when the liabilities are paid off. It is the total assets minus the total liabilities. Subdivisions of Owners Equity: -Drawings:The money the owner withdraws from the company -Capital:The claim to the company of the owner -Revenue:The money made from sales -Expenses:The costs required to earn revenue

Income Statement -A statement that shows the change in a company's financial position during a period.

Claims Against Assets -Owner's and creditor's, people who are owed money, claim on a company's assets. The creditors are payed first if a business is sold or closed down and the owner get the rest of the money.

Business Transaction -The business exchange of money, service or goods between multiple parties.

Source Documents -Documents or papers that confirm the transactions of a business and amount of money exchanged.

Balance Sheet Equation -A equation that states total assets equal the sum of total liabilities and owner equity. It makes sure the assets, liabilities and equity are in balance.

Business Entity Concept -The accounting for a business must be separate from other businesses or the owner's personal affairs.

Cost Principle -The value of assets must be recorded at the cost when they were originally purchased, disregarding current market value.

Going Concern Concept -It is assumed the business will continue to operate unless it is known it will stop operating. If a business is closed then the value of the assets are determined once sold.

Principle of Conservatism -The accounting of a business has to be fair and reasonable and the numbers on a report has to be realistic.

Transaction Analysis -The studying and recording of the changes in the financial position of a business.

DR/CR Theory -Debits are on the left side and Credits are on the right side. Assets are on the left side of balance sheets so the beginning value and increases are on the left side and the decreases are on the right side. Liabilities and Owner's Equity are on the right side of balance sheets so the beginning value and increases are on the right side and the decreases are on the left side.

Ledger -A collection of accounts that are the same type.

Account Balance -The amount of money currently in an account. Normally Assets have a debit balance and liabilities and owner's equity have a credit balance. Exceptional balances are when the amounts are on the opposite side. That means the accounts have a negative balance.

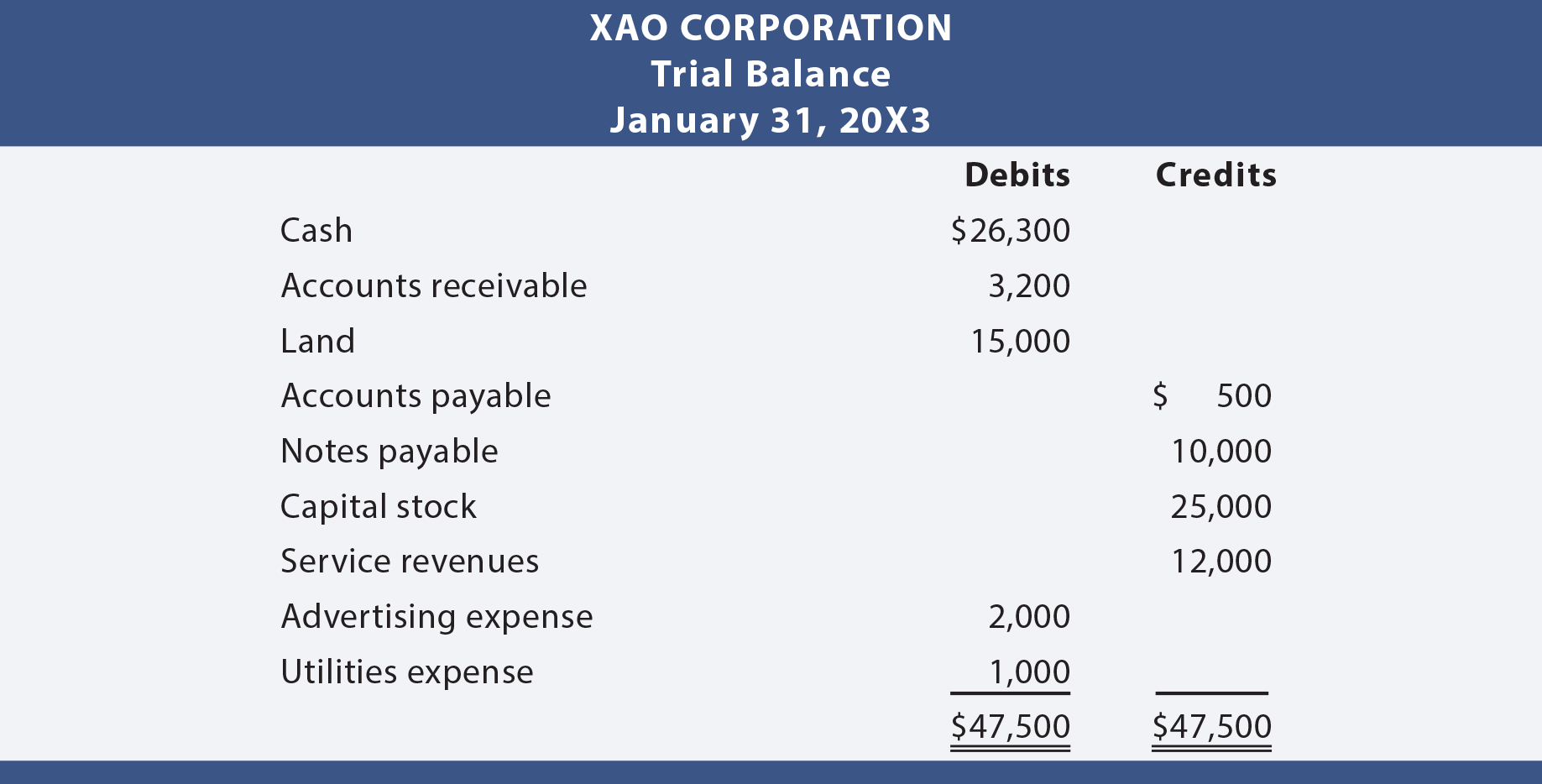

Trial Balance -A sheet that lists the accounts of a company and shows the debit/credit balances for the accounts. It is used check if the ledger is correct.

Equation Analysis Sheet -A sheet that shows the transactions and the change in financial position after each transaction. The amounts on a balance sheet are usually used as the beginning amounts for the equation analysis sheet. It is used to make corrections if the balance sheet is not in balance.

T-accounts -Financial records that show the transactions of individual accounts with a chart in shape of a T. The left side is the debit side and the right side is the credit side.

Time Period Concept -Accounting happens in specific time periods. Those periods are called fiscal periods.

Accounting Regulations -Rules and regulations accountants have to follow. The standards for accountants in Canada are mostly established by Canadian Institute of Chartered Accountants (CICA). The CICA Handbook has all needed accounting knowledge and is regularly updated.