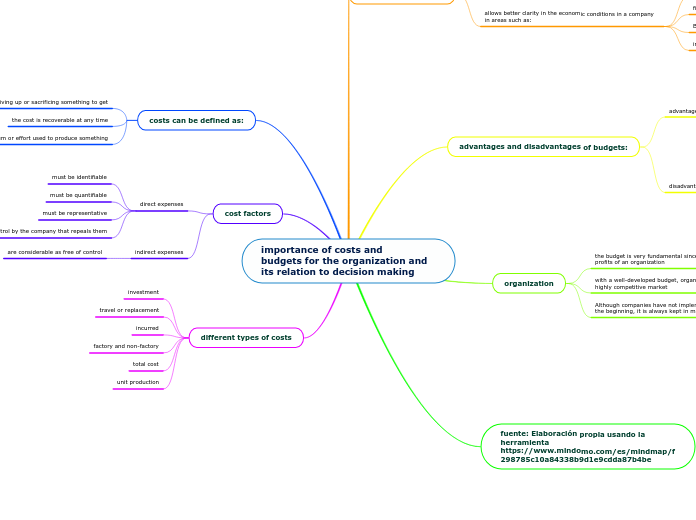

importance of costs and

budgets for the organization and its relation to decision making

costs can be defined as:

the cost of giving up or sacrificing something to get

the cost is recoverable at any time

the sum or effort used to produce something

cost factors

direct expenses

must be identifiable

must be quantifiable

must be representative

there is a control by the company that repeals them

indirect expenses

are considerable as free of control

different types of costs

investment

travel or replacement

incurred

factory and non-factory

total cost

unit production

budget is defined as:

It's a financial plan designed to guide the

businessman to get the targets of the proposed goals

historical data is essential when making a budget

involves materializing business plans in quantitative and monetary information

allows better clarity in the economic conditions in a company in areas such as:

indebtedness

financial liquidity

Bank transactions

investments

allows to determine if the company has the capacity to develop the planned activities

advantages and disadvantages of budgets:

advantages

provides financial information for the company to generate competitive results

allows clarity regarding the sales, costs and expenses that each department of the company must meet

disadvantages

implementation is expensive and time consuming

requires commitment from all levels of the company for its proper functioning, which is not always possible

some admins take the budget very strictly, which does not allow new financial alternatives to be explored

organization

the budget is very fundamental since it controls and plans the profits of an organization

with a well-developed budget, organizations can remain in a highly competitive market

Although companies have not implemented a budget plan from the beginning, it is always kept in mind when making decisions