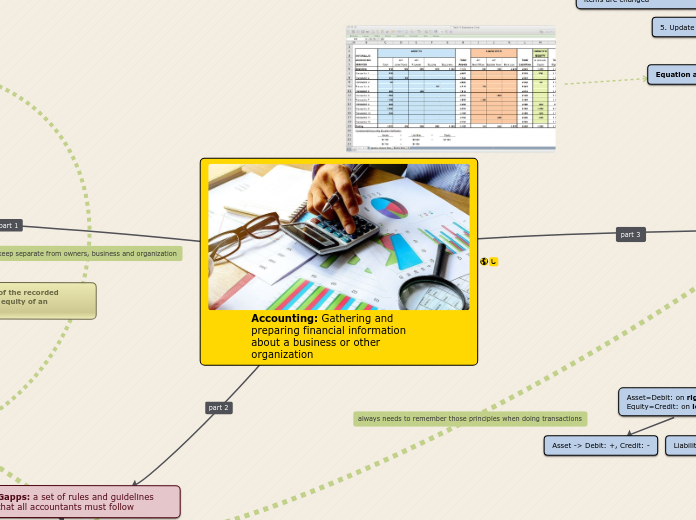

Accounting: Gathering and preparing financial information about a business or other organization

Accounting Concept

Financial Position

The current balances of the recorded assets, liabilities, and equity of an organization

Claim Against the Assets

Creditors (Called liabilities)

Owners (Called owner's equity)

Types of Business

Service business

Only sell services to customers, provide intangible things instead of physical and durable things. Provided by skilled people

Ex: accounting firm; catering company; cinema; teacher; doctor, etc

Merchandising business

Sell physical items (buy from a manufacturer)

Ex: clothing store; department store; grocery store, etc

Manufacturing business

Buy raw materials and manufacture goods

Ex: computer manufacturer; food-processing company,etc

Non-profit business

Businesses that do not earn money

Ex: charities; amateur sports organization; curches, etc

Forms of Ownership

Sole proprietorship

Business that owned by a single person

Ex: Dr.Joe Dimitry; Dentist

Partnership

Business that owned by two or more partners, share responsibilities and costs

Ex: McPearson & Scott Charterd Accountants

Corporation

Highly regulated by provincial and federal government

Ex: Business names that include Inc (Incorporated), Corp(corporation) or Ltd(limited)

Gapps: a set of rules and guidelines that all accountants must follow

Key principles

Business Entity concept

Keep separate from the personal affairs of owner, other business or organization

Ex: Business owner can use money for personal things

Cost Principle

Record the value as the purchase price.

Ex: If your company used $30 to buy an item, but one day later, it changed to $40, you need to record the money as $30 as this is how much you pay to buy it.

Objectivity Principle

Provide objective evidence

Ex: You can not say this dessert is the most delicious one in the world because that's probably not correct.

Matching Principle

Each expense item related to revenue earned must be recorded in the same accounting period as the revenue it helped to earn

Ex: If a bought a thing in 2019 but no one use it until one year later someone use it to make money/do things, then the expense should be recorded 2020.

Consistency principle

Once you adopt an accounting principle or method, continue to follow it consistently

Full Disclosure Principle

All information needed for a full understanding of a company’s financial statements must be included with the financial statements

Time Period Concept

Consistent time periods

The global standard time periods are monthly, quarterly and yearly.

Revenue Recognition Principle

Revenue must be recorded when the transaction was complete

Principle of Conservatism

Accounting for a business should be fair and reasonable

Ex: You can't say your business worth 1,000,000,000 dollars when you just get started because that's impossible.

Going Concern Concept

Assumes that the business will continue to operate unless it is known that it will not

Fundamental Accounting Practices

Balance sheet: shows the

financial position of an individual,

company, or other organization on a

certain date.

Steps to create a balance sheets

1. Write the heading: Who, What, When.

2. List all the assets under the assets subheading

3. List all the liabiities under the liabilities subheading

4. Total the liabilities with a ruled line

above the total.

5. Calculate Owner's Equity

6. Calculate the total Assets and total Liabilities and Equity on a same line with a ruled line (they should be same amount)

7. Put two ruled line below the two totals

8. Add dollar signs to the first number in each

column, the total assets, and the total liabilities

and equity.

Correct order

Assets

Order of Liquidity

Order by useful

life

Liabilities

Due day: list what you need to pay first at first

Fundamental Accounting

Equation

Assets = Liabilities + Owner’s Equity

Assets – Liabilities = Owner’s Equity

Assets: Resources (things) owned by a business

Ex: Cash, Accounts Receivable, Supplies, Equipment, etc

Liabilities: Things the company owes

Ex: Acounts Payable, Bank Loan, Mortgage

Owner's Equity: The difference between our

assets and our liabilities

Ledger: All accounts put together

Debit credit theory

Double Entry Theory

First entry debit, second is credit

Total debit entry=Total credit entry

Asset=Debit: on right; Liability=Owner's Equity=Credit: on left

Asset -> Debit: +, Credit: -

Liability/Owner's Equity -> Debit: -, Credit: +

T-account

Steps(Assets on left; Liabilites & OE on right in the beginning)

1. Write the names of accounts

2. Record the initial amount for each account

3. Record the transactions

Account Balance

Dollar value of an account and shows whether it is a debit or a credit

First record all the transactions on T-account, then subtract the smaller total from the larger total. Write the result under the larger of the two pin totals.

Exeptional Balance (an account ends up with a balance opposite to its normal one)

Ex: overpay an account payable; Customer overpays account balance, etc

Trial balance

Debit = Cedit -> in balance

Debit != Credit -> not in balance

Business transaction: cause the

financial position of a business to

change (per event per transaction)

Source Document

Business paper

Ex: Invoice, Telephone bill, cheque

copies, store receipts

Equation analysis sheet

Steps

1. Write down the fundamental accounting equation and list the items in the assets, liabilities, and owner’s equity sections

2. Record the initial balances from its corresponding balance sheet.

3. Start record each transaction

4. Make sure each transaction has two individual items are changed

5. Update the balance sheet

On accounts

Purchased on credit

Assets and A/P

Sold on credit

A/R and Capital

Payment on account

A/P and Bank(cash)

Receipt on account

A/R and Bank(cash)